Spotting Opportunities and Risks Across the EM Investment Universe

Similar to stargazers, investors can benefit from looking through a variety of lenses to form an overall picture. Three lenses commonly used to evaluate investments are valuations, technical factors, and fundamental characteristics, and the relationship among the three can vary throughout a market cycle.

In emerging markets (EM), valuations – which assess what an asset is worth relative to similar securities, historical norms, and future expectations – look attractive today after the losses across financial markets early this year. EM option-adjusted spreads were recently in the 98th percentile of levels observed over the past 20 years, according to JPMorgan EMBI Global Index data as of 29 July 2022.

Yet EM remains susceptible to technical factors, which include a market’s trading dynamics and shifts in investor sentiment. This year has produced the worst EM fund outflows on record, according to Emerging Portfolio Fund Research, and EM remains vulnerable as the U.S. Federal Reserve and other central banks raise interest rates in an attempt to fight inflation without inducing a recession.

As the outlooks for inflation and monetary policy become clearer, EM could be poised to rally. At that point, fundamentals – which assess the underlying financial picture and creditworthiness of a company or country – can become more important differentiating factors. In EM, those differences can be key for investors, because country-specific risks can balloon more quickly and unexpectedly than risks in other credit-related sectors. Here, we explore some areas of EM that may show signs of heightened risk today.

Locating gravitational distortions

PIMCO’s investment process is founded upon our macroeconomic outlook and our in-house country and credit research. To further guide that process, PIMCO has developed a “black hole risk” framework that aims to identify and avoid extreme, country-specific situations where the first price decline may not signal a buying opportunity but rather a gateway to further declines, creating a gravitational spiral that offers investors no escape.

A careful approach to country and security selection can help anticipate disruptions such as credit-rating downgrades, political turmoil, policy changes, imposition of capital controls, or sovereign debt defaults. Our risk framework looks at factors including inflation, GDP, debt and deficit levels, currency reserves, corporate and banking sector risks, and external financing availability.

We also incorporate qualitative factors including politics, election scenarios, social demands, and other sources of latent risk, such as foreign exchange misalignment, implicit sovereign contingent liabilities, and geopolitics. This creates a dashboard of early warning indicators for sovereign credit risk related to debt burden, liquidity, financial imbalances, and qualitative variables that could eventually lead to bond restructurings or currency devaluations.

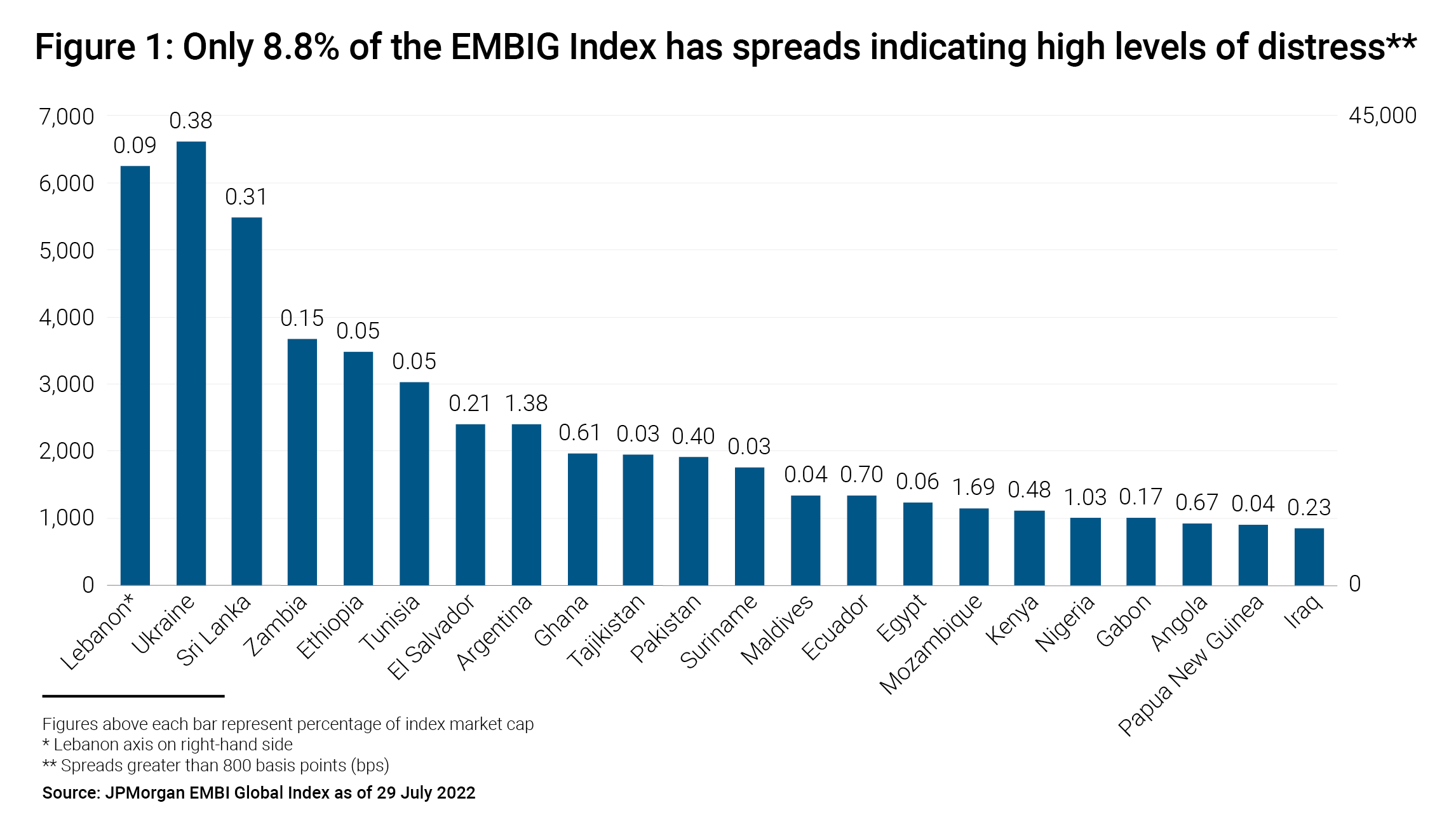

Looking at that dashboard today, the good news is that EM fundamentals broadly appear sound, but those fundamentals could deteriorate in a select few countries. Less than 9% of the debt in the JPMorgan EMBI Global Index by market capitalization trades at spreads indicating elevated levels of distress (see Figure 1).

Identifying the most at-risk segments of the index can help investors make more prudent and defensive decisions, such as not reaching for yield by taking on extra credit risk in a particular country. Our framework aims to spot countries at elevated risk so we can designate them and handle them with care in advance – for example, Sri Lanka in 2020, well before the country defaulted on its debt two years later.

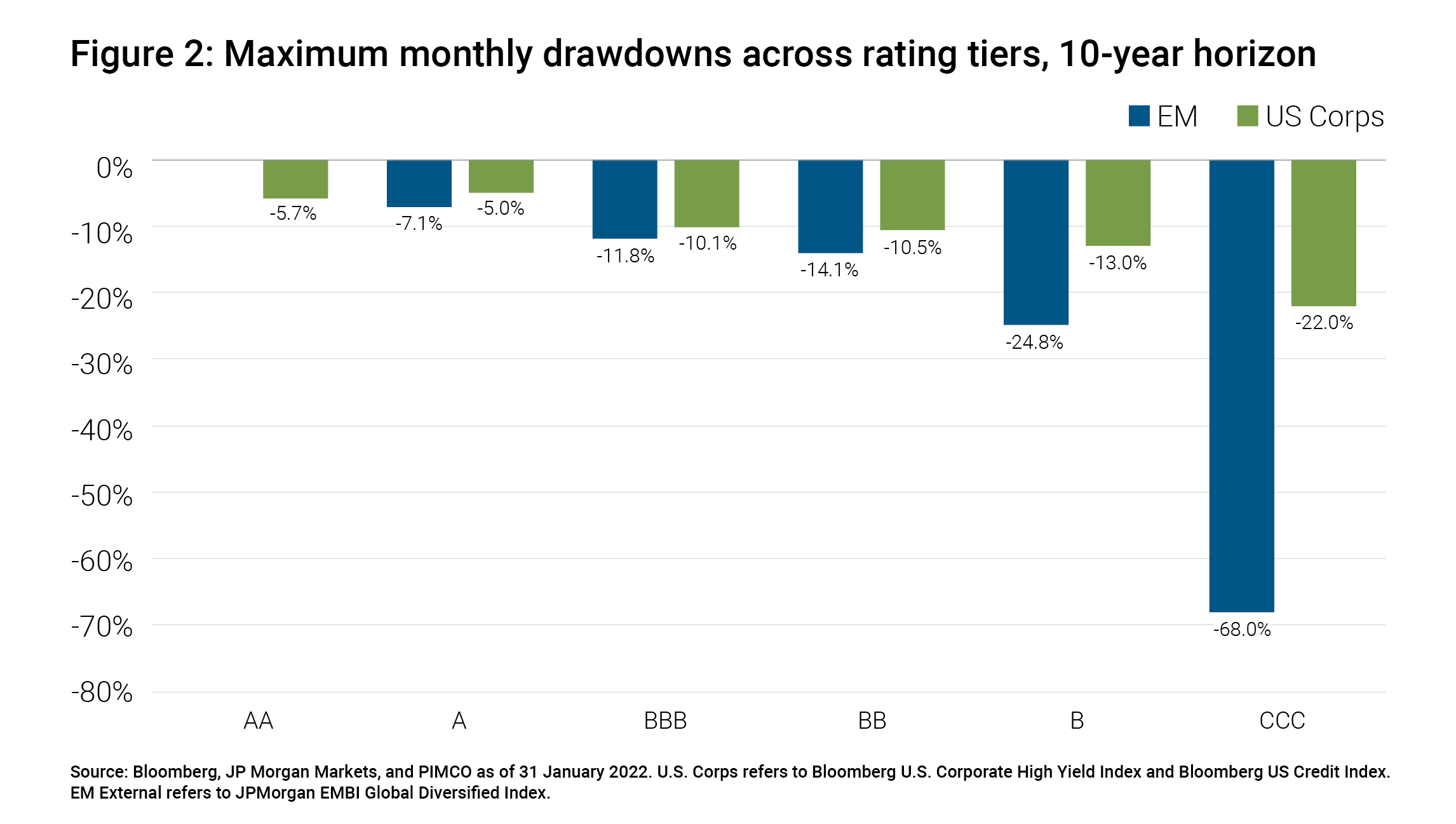

Although lower-quality frontier markets can appear to offer great value, investors should exercise caution given the degree of risk involved. Historically, the lowest tiers of EM credit ratings have experienced higher default rates (12.2%) than similarly rated developed market corporate bonds (9.3%), according to Moody’s. Similarly, the lowest rating tiers of EM debt have been subject to sharper periodic drawdowns than U.S. corporate debt (see Figure 2).

It’s often wise to avoid the temptation to get too bullish on any particular country, because the broader technical backdrop in EM can at times overpower fundamentals. Focusing on downside risk mitigation can help smooth the journey in what can be a volatile asset class. While EM valuations have become more compelling, especially for some lower-quality issuers, we prefer to wait for more clarity around current global headwinds before pivoting to a more bullish stance.

To learn more, visit PIMCO’s Emerging Markets site .

Pramol Dhawan leads emerging markets portfolio management, and Lupin Rahman leads emerging markets sovereign credit portfolio management.