Summary

- Defined benefit (DB) plan sponsors seeking to outperform liabilities can either allocate more to return-seeking assets or employ a higher degree of active risk within their liability-driven investing (LDI) portfolios.

- When properly defining risk, return and costs, we believe that active management of LDI assets handily beats further allocations to return-seeking assets on the efficiency scale, and thus a higher active risk LDI approach potentially leads to better risk-adjusted outcomes.

- Plan sponsors should evaluate whether they are getting enough from their LDI portfolios and make changes where appropriate.

It’s been widely accepted that active approaches are essential to managing U.S. liability-driven investing (LDI) portfolios, but there is far less consensus about how much active risk and alpha to target. In recent years, a growing number of market participants have advocated for lower active risk (i.e., less discretion and a lower alpha target) in LDI portfolios. We disagree – and encourage plan sponsors to consider a higher active risk LDI approach.

The argument for lower-discretion LDI typically revolves around three themes:

- LDI is first and foremost a risk-reduction exercise.

- Therefore, the amount of active risk in LDI portfolios should be relatively low.

- Plan sponsors should thus rely on their return-seeking allocations for generating returns in excess of liabilities.

This narrative may sound straightforward and effective. However, a more thorough analysis of risk budget optimization for defined benefit (DB) plans suggests it doesn’t hold up. In fact, this narrative may have it backward. We believe that a more significant amount of active risk in LDI portfolios is the most efficient way to reduce asset-liability risk since it potentially enables plan sponsors to achieve return targets with a lower emphasis on return-seeking asset classes.

Reducing the “cost” of outperforming liabilities

The large majority of plan sponsors seek to outperform their liability return (or its growth rate). Doing so can help reduce a funding deficit, build a surplus cushion, overcome the high hurdles set by uninvestable liability discount rates or offset potential costs associated with improvements in longevity. DB plan managers have a range of options to target returns in line with their objectives.

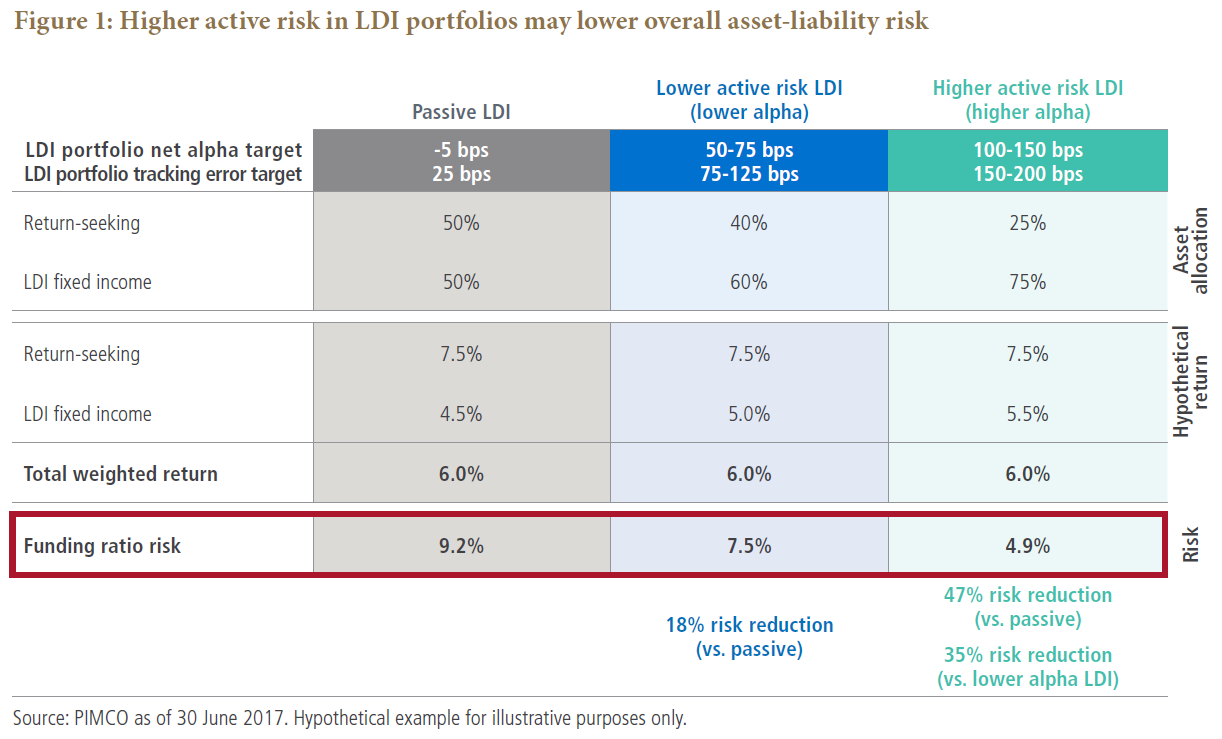

At one end of the spectrum, Figure 1 shows that a plan sponsor targeting a 6% expected return could allocate 50% of assets to a passive LDI strategy and 50% to a return-seeking portfolio. Based on hypothetical return assumptions, this combination would meet a 6% estimated return target. Allowing for a moderate amount of active risk in the LDI portfolio (with a net alpha target of 50 basis points (bps)) achieves the same return target with a lower allocation to return-seeking assets (40% return-seeking/60% LDI). Finally, targeting a higher amount of net alpha in the LDI portfolio (100 bps in this example) enables the sponsor to maintain the same 6% return target while lowering the return-seeking allocation to 25% (25% return-seeking/75% LDI).

While all three approaches target the same return, the higher alpha LDI approach (in green) conveys significantly lower funding ratio risk. This invalidates the assertion that low-discretion LDI portfolios are optimal for plan sponsors seeking to limit asset-liability risk.

The low-discretion LDI narrative leads to the wrong conclusion because its definition of cost is too narrow. With this approach, the focus has been to reduce costs by lowering investment management fees on the LDI portfolios. Indeed, targeting a lower active risk budget (and ultimately lower alpha) on LDI portfolios may achieve that narrow objective.

However, a more comprehensive assessment of “cost” shows the fallacy of this reasoning. A lower-discretion approach may save a few basis points in fees, but it also requires the plan sponsor to maintain a larger return-seeking allocation to achieve its desired return target. In the final analysis, the incremental asset-liability risk resulting from the higher return-seeking allocation is a direct and more significant potential cost to the plan sponsor than the few basis points saved in management fees for LDI portfolios.

In other words, the “cost” of generating excess return over the liabilities – if “cost” includes the potential incremental risk relative to liabilities – is much lower for active management of LDI portfolios than for a higher equity (or other return-seeking) allocation.

Thus, to optimize their risk budget, plan sponsors should seek as much added value as they reasonably can from their LDI portfolios to reduce the required allocations to return-seeking asset classes – even if that means paying slightly higher fees on LDI portfolios.

A wider view

Several other considerations support the idea of allowing more discretion and targeting higher excess returns in LDI portfolios.

Mitigating downgrade and demographic risk

Bond universes used to construct most liability discount curves have specific criteria for credit quality. However, discount curve methodologies are fairly lenient when it comes to the treatment of downgraded securities. For instance, when a bond is downgraded and ceases to meet the quality criteria, it is simply removed from the universe used to construct the curve. Therefore, while a passive liability-matching portfolio typically incurs a hit due to the downgrade event, the liability will most likely go up on the news, all else being equal. (The reason is that one of the lowest-quality, and thus highest-yielding, bonds no longer factors in to determining the average discount rate; the discount rate then falls, sending the liability higher.)

In addition, over the long run, pension liabilities may grow at a pace that exceeds their discount rate if life expectancy improves faster than expected.

Therefore, plan sponsors may need a significant amount of alpha from their LDI portfolios just to keep pace with the growth in liabilities — and ensure that any return-seeking portfolio outperformance really goes toward improving their funding ratios as opposed to making up the potential shortfall resulting from a lower active risk LDI approach.

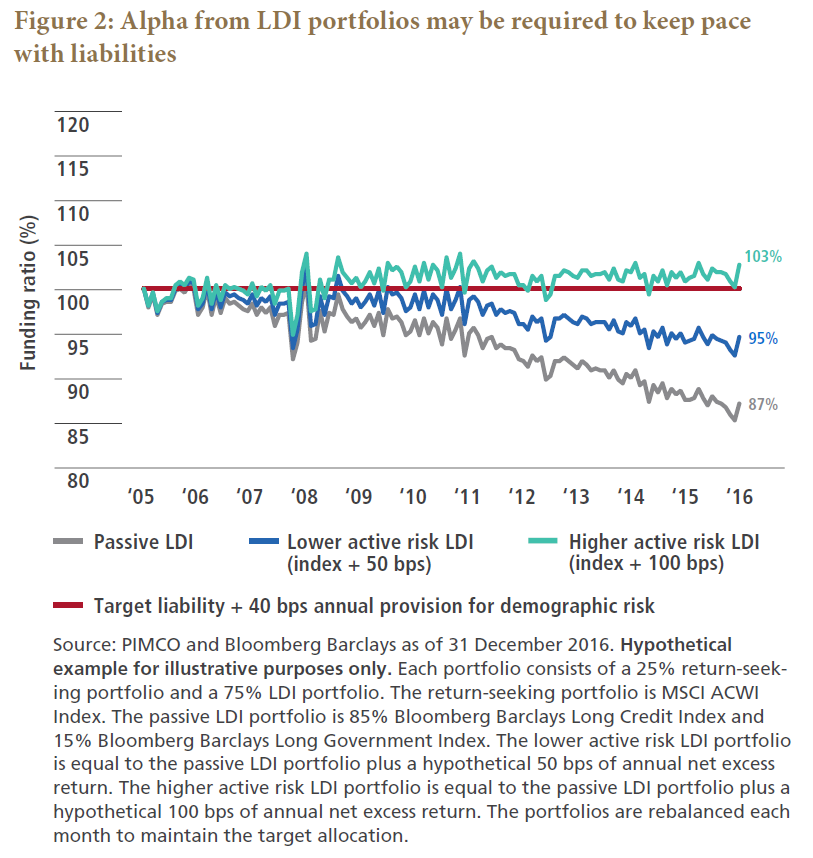

As Figure 2 shows, over the last decade a DB plan would have needed almost 100 bps of net alpha to keep pace with liabilities. That level of excess return is more consistent with a higher active risk portfolio than with the lower-discretion approaches that have gained favor recently.

Lowering plan contributions

Pension deficits can potentially be reduced (or surplus cushions built) either through the outperformance of assets versus liabilities or by contributions to the plan. As such, forfeiting potential asset outperformance is likely to translate into higher plan contributions down the road.

Liability-risk management considerations, of course, limit the extent to which allocations to return-seeking assets can be dialed up to target excess returns over liabilities. Thus, allowing for higher active risk within LDI portfolios can help plan sponsors potentially reconcile the dilemma between the desire to achieve lower contributions (via higher returns) and the need to control funding ratio risk.

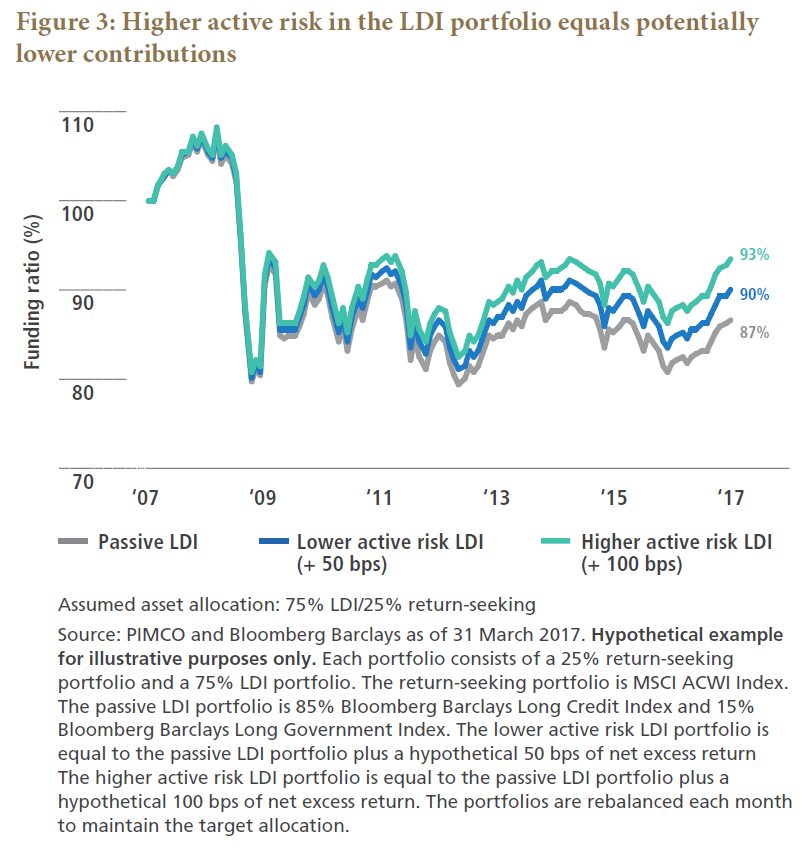

Ultimately, a healthier amount of alpha earned in the LDI portfolio can generate significant contributions savings. As an example, Figure 3 shows the evolution of funding ratios of hypothetical plans over the past 10 years. The plans had identical allocations: 75% to LDI and 25% to return-seeking assets. In the plan represented by the green line, the actively managed LDI assets generated 100 bps of alpha; with the plan represented by the blue line, the active LDI portfolio generated 50 bps. Over the 10-year period, the plan with the higher active risk LDI approach achieves a funding ratio three percentage points higher than the plan with the lower active risk LDI portfolio (93% versus 90%) and six percentage points better than the passive allocation. This translates into $30 million and $60 million in contributions savings, respectively, per $1 billion of liabilities.

Employing a more active LDI approach may result in negligible incremental risk

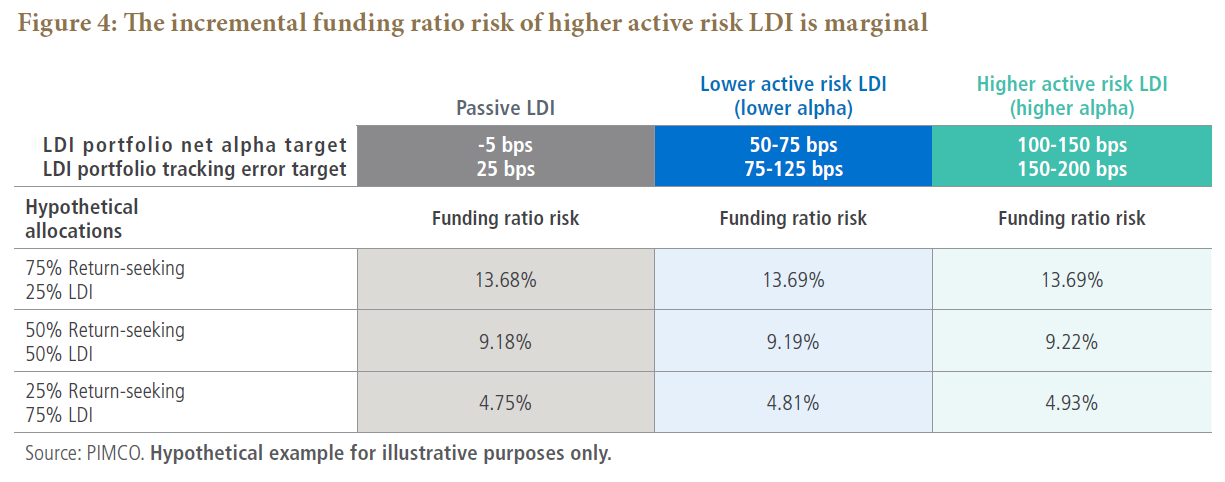

When assessing and quantifying the incremental risk of active management in LDI, investors sometimes focus on tracking error relative to the portfolio benchmark. For example, the second row in Figure 4 would suggest that the incremental tracking error of the higher active risk approach is about 75 bps greater than the lower active risk LDI approach (as the LDI portfolio tracking error increases from a range of 75-125 bps to 150-200 bps). Yet this assessment takes too narrow a view of portfolio risk, especially in the asset-liability context.

The variables that most plan sponsors care about (funding ratio, contributions, pension expense, etc.) are driven ultimately by the relationship between total assets and liabilities – and not by the relationship between the LDI portfolio and its benchmark in isolation. And when looking at the incremental risk of a more active LDI portfolio through that lens, the added risk of a higher-discretion LDI portfolio becomes negligible (see rows 3-5 in Figure 4). This is because the incremental risk in LDI portfolios gets diversified away by other uncorrelated portfolio beta risks and liability risks.

Get more from your LDI portfolio to reduce risk

Outperformance of assets relative to liability returns is either a necessity or a very desirable outcome for an overwhelming majority of DB plan sponsors. Given the wide range of options to structure a pension portfolio with an expected return in line with the sponsors’ target, consequential decisions will need to be made in an effort to optimize the plan’s risk-return trade-off. Among these, defining the acceptable degree of active risk in LDI portfolios may be the most important.

When properly defining risk, return and costs, we believe that active management of LDI handily beats further allocations to return-seeking assets on the efficiency scale, and thus a higher active risk LDI approach is likely to lead to better risk-adjusted outcomes. Plan sponsors should therefore evaluate whether they are getting enough out of their LDI portfolios and make changes where appropriate.

With the prospect of lower future returns across return-seeking asset classes, there has never been a better time to go through this exercise.