After two years of interest rate volatility that tried many advisors’ nerves, the outlook for bonds appears the healthiest we’ve seen in years thanks to two key factors: Starting yields are near their highest levels in more than a decade, and the Federal Reserve is expected to start easing policy this year.

Of course, advisors are understandably cautious. The historic rate rise in 2022 led to negative returns in most fixed income sectors. Advisors then started moving cash off the sidelines in 2023 and 2024 as yields reset at healthier levels – only to encounter renewed volatility.

However, history suggests that today’s starting conditions should add up in bond investors’ favor.

This content is provided for educational purposes only and should not be viewed as investment advice or as an offering of any product or strategy. Consult your financial professional for more information.

A compelling entry point

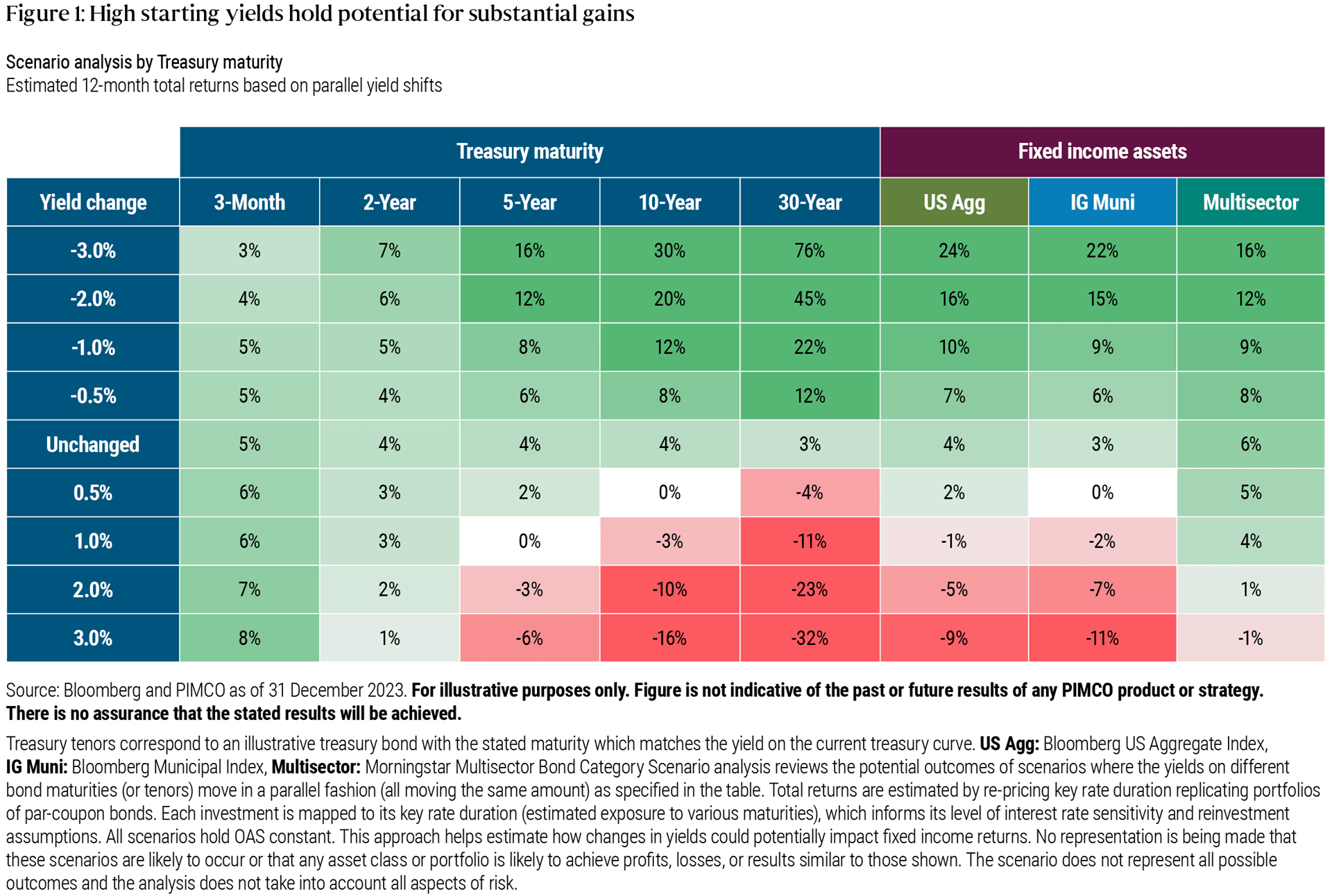

The compelling nature of today’s fixed income entry point is demonstrated in Figure 1, which outlines the potential returns across various fixed income sectors based on current yields and illustrative interest rate movements. This analysis reveals that current starting yields may help anchor return potential for bonds at attractive levels, while also providing a cushion against any further increases in interest rates.

For example, in the multisector bond category below, if 2024 follows a similar path as 2023 and rates end where they start, return expectations are a healthy 6%. If rates rise, they would need to hit nearly 7% (an increase of over 200 basis points (bps)) to turn estimated multisector returns negative.

Categories with more duration, or interest rate sensitivity, such as core bonds and investment grade municipals, may also offer a compelling trade-off. Unlike 2022 when starting yields were much lower, returns today are likely to remain positive even with modest further increases in rates. However, if rates fall even 1 percentage point, returns could climb into double digits.

The one category that shouldn’t benefit from falling rates? Cash investments, as a decline in short rates can quickly translate to a decline in investor returns. That’s not to mention the potential opportunity cost missed by not participating in the drop in interest rates and the likely rally one would experience across most fixed income sectors.

Starting conditions matter

Last year was a clear reminder of the pivotal role that high starting yields play in mitigating downside risks and driving positive returns in fixed income. Despite the significant move in rates intra-year with the 10-year yield briefly touching 5% in October, many yields further out on the curve ended the year roughly where they began. In fact, the 10-year yield started and ended the year at exactly the same level of 3.88%.

That round trip in yields allowed bonds to end 2023 on a high note, with returns in the mid to high single digits, as starting yields drove attractive returns. In fact, across most major fixed income sectors, a majority of 2023 returns were driven by yield as opposed to price movements.Footnote1 The rally in interest rates in November and December simply erased price losses from rising rates earlier in the year.

Additionally, though rates rose through October, most fixed income sectors remained positive or only dipped modestly into negative territory as income from higher yields helped offset price losses. That was not the case in 2022, when much lower starting yields and stronger movements in interest rates and spreads drove most fixed income sectors into negative territory. Importantly, looking forward, starting yields in 2024 are much closer to the high levels of 2023 than the lows of 2022. For example, while the yield on the Bloomberg US Aggregate Bond Index stood at 1.70% to start 2022, those levels were 4.65% and 4.52% to start 2023 and 2024, respectively.

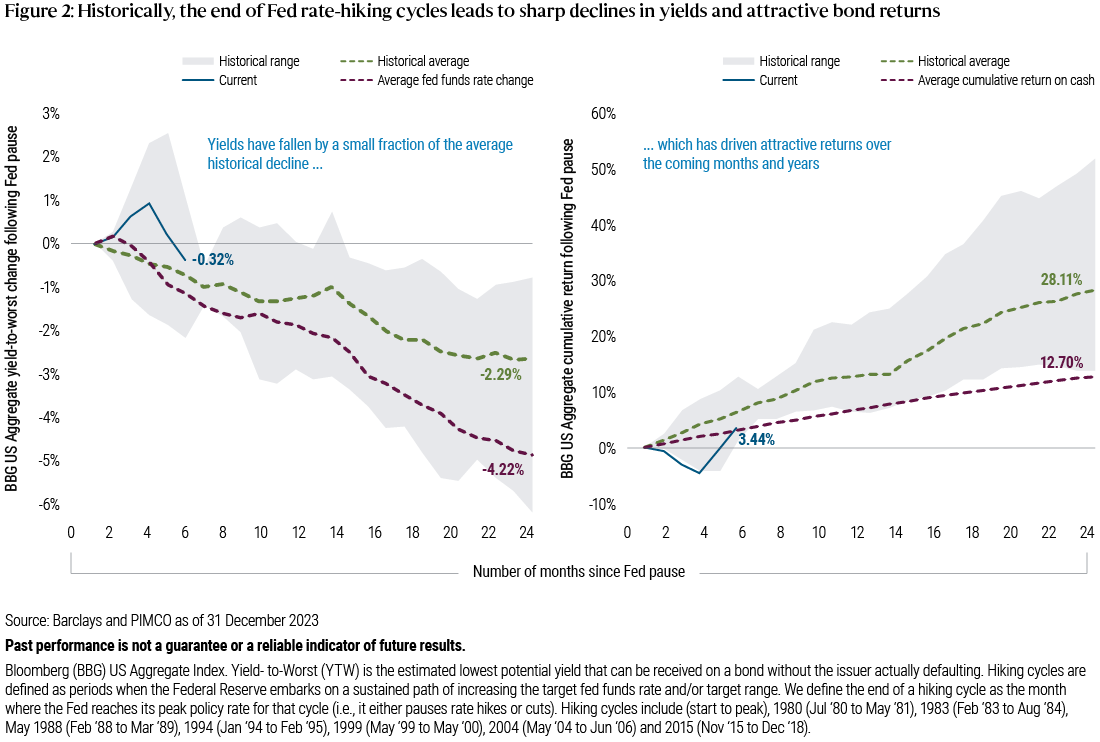

Based on history, bonds may still have considerable upside

History suggests we may still be in the early innings of a bond market rally. As Figure 2 shows, over the last seven Fed rate-hiking cycles since 1978, bond market rallies have tended to last more than a year or two after the final hike.

Additionally, as the Fed begins to ease, front-end yields have tended to fall significantly, which hinders cash returns. Meanwhile, even modest declines in interest rates at longer maturities have tended to lead to notable outperformance for fixed income portfolios due to the price appreciation that falling rates provide.

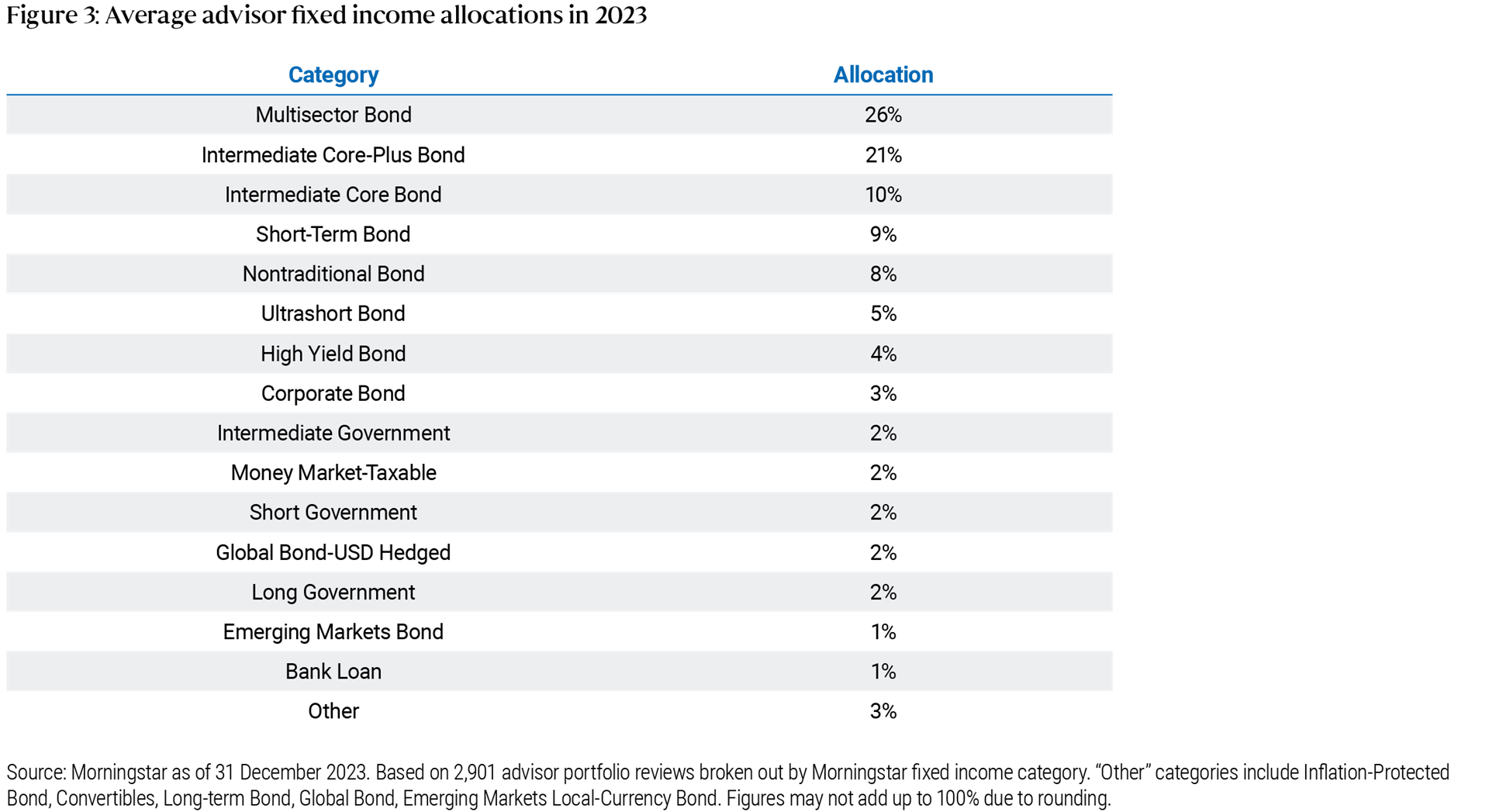

A review of advisor fixed income positioning in 2023: starting to move cash off the sideline

Over the past two years, many investors boosted cash balances – as evidenced by record levels of assets in money market funds, CDs and bank deposits. But with the Fed likely paused before the expectation of rate cuts later this year, it is a logical time to revisit elevated cash holdings.

Indeed, as yields reached attractive levels, our conversations with advisors in 2023 explored how they could consider increasing allocations to bonds in pursuit of higher returns, while better balancing risks in their fixed income allocations. A review of the allocations of the average advisor portfolio we evaluated in 2023 as shown in Figure 3 highlights a few key themes:

- A balance between core and multisector strategies continued to anchor portfolio allocations.

- Allocations in short-term categories fell by about 5% from 2022 as advisors started to redeploy these assets into longer-maturity fixed income allocations.

- Interest in active fixed income strategies rose given continued market volatility.

Looking ahead

While short rates are higher and cash-equivalent investments may remain attractive in the near term, we believe fixed income looks to be the more compelling long-term investment. Yields across most fixed income sectors are at attractive levels rarely seen in the last twenty years. Additionally, compared with last year, the prospect of falling rates could provide an additional tailwind to bond returns.